The Disruptive Potential of Buy Now Pay Later in Western Europe

18 July 2022

FEATURED ARTICLE

Since the outbreak of the COVID-19 pandemic and the subsequent surge in e-commerce in Western Europe, ‘Buy Now Pay Later’ (BNPL) as a short-term financing alternative has been catapulted into the mainstream. As early movers, the rising number of financial technology (fintech) players, which face limited regulatory constraints, have driven this development, outpacing entrenched companies. Although still accounting for a small overall share in consumer finance, its growth trajectory and how BNPL is changing the nature of lending and payments highlight its disruptive potential.

The appeal of BNPL

The concept behind BNPL, of splitting the cost of purchases into instalment payments spaced out over a predetermined period of time, is in essence not completely new, in view of credit card lending and non-card lending via banks and retailers. However, emerging fintech players have significantly simplified and improved the process from a consumer perspective. BNPL allows users to make purchases without traditional financing requirements such as comprehensive credit checks or high credit card interest rates. In fact, many players offer no-cost financing, both online and at the physical point of sale.

Source: Euromonitor International’s Passport Retailing data, 2022 edition

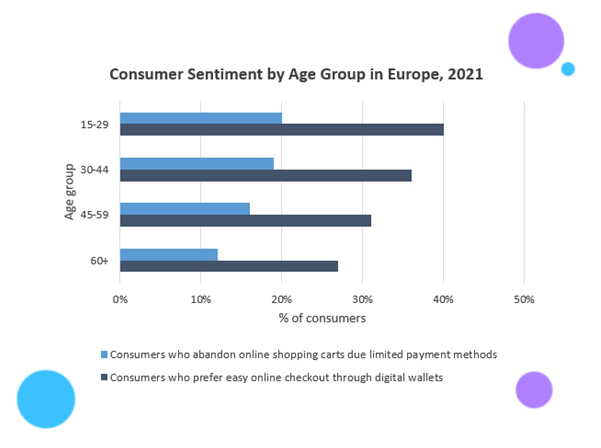

This has resonated with consumers across Western Europe, especially with tech-savvy millennials and gen Z, who have fuelled demand, particularly amid the surge in online shopping as a result of the COVID-19 pandemic. Young consumers with limited incomes value the service as an alternative digital payment and lending option with flexible instalment plans, enabling them to easily purchase big-ticket items. Yet increasingly, the service is also seeing growing popularity for small items. As a result of its rising popularity, there are rising concerns that BNPL raises the risk of unsustainable levels of consumer debt.

Source: Euromonitor International’s Voice of the Consumer: Digital Survey, fielded in March 2021

Retailers also have a strong incentive to integrate BNPL as an additional payment option. By paying a fee to the BNPL provider to offer the service, merchants enjoy numerous benefits in return. Retailers receive the purchase amount, minus fee, immediately, thereby removing the risk of default. Moreover, with the ability to break up their total purchase into instalments, consumers are more open to impulse purchases and tend to spend more than they would if they had to pay the whole amount at once, resulting in higher sales. In turn, higher convenience and customer satisfaction can result in improved customer acquisition, strengthened loyalty and higher conversion rates. In addition, since BNPL weakens price as the decisive purchasing factor, the service also has an impact on the competitive landscape, not least for players not offering BNPL.

Early movers reap the benefits of BNPL’s growing popularity

In Western Europe, the BNPL market is primarily dominated by players from the relatively new fintech industry. Both global and local players are present, but products, features and geographical presence differ player by player.

Source: Euromonitor International

The popularity and potential of the BNPL model attracts the fintech segment to join the competition. Three challenger banks, Revolut, Monzo and Curve, recently announced their plans to offer this payment solution. Linking their new BNPL products to their already existing cards is likely to provide them with a competitive advantage in the BNPL space. They might be able to reach more users thanks to their already existing customer base, not to mention brand awareness and trust.

Profound impact on the region’s consumer finance landscape expected

From the consumer perspective, BNPL providers offer a superior customer experience compared with traditional credit solutions, driven by their real-time financing approval processes, often without interest. Therefore, the service has rapidly changed how consumers shop online and in-store, leading to growing pressure on traditional credit providers. Thus far, fintechs have dominated BNPL thanks to recognisable brands that resonate especially with the younger generations. While this leaves banks with a reduced market share among new-to-credit customers, it also highlights the risk of a broader decline in competitiveness vis-à-vis fintechs. Moreover, with its growing use for smaller purchases, BNPL also puts increasing competitive pressure on credit card operators. BNPL offers a simple and cheaper digital alternative, thereby significantly reducing the incentive for young consumers in particular to consider credit cards. This is further amplified by retailers promoting BNPL as the most attractive payment solution. Therefore, on balance, the ongoing rise of BNPL is likely to attract significant consumer lending volumes at the expense of traditional products in Western Europe in the years ahead.

New regulation could limit the level of disruption

Easy accessibility has been a contributor to the success of BNPL, which is due to the absence of regulation around offering and using this model. Currently there are no hard credit checks for point-of-sale financing in Western Europe. However, the rapid evolution of the model and the booming demand for BNPL raises concerns around the unregulated provision of credit. The Financial Conduct Authority (FCA) in the UK has named the key risks the model holds for consumers and the wider credit market. These include, but are not limited to, the lack of information for consumers around the features of BNPL, the lack of consumer creditworthiness assessment, and the potential creation of over-indebtedness.

While BNPL has a stronger presence in more digitally advanced markets such as the UK, Europe-wide regulation is expected to come into effect in 2022 or 2023. In 2021, both the FCA and European Commission submitted proposals for the regulation of this popular payment model. Legislation would not only advocate consumer protection, but also fair competition. Regulation would also allow mainstream credit providers, which have been finding replicating BNPL products difficult, to compete more closely with fintechs. However, cutting the margins of BNPL provider fintechs would impose significant threats on the current leading providers. Although regulation would aim not to adversely impact innovation in the industry, it raises questions around the future existence of the current form of the popular BNPL model. The potential introduction of strict credit checks and compulsory interest rates might result in declining consumer interest in the model, and would also challenge the financial sustainability of pure BNPL providers.

Key takeaways for industry stakeholders going forward

The outlook for the BNPL model in Western Europe is highly dependent on the nature of legislation which comes into effect in the next year or so. However, if the model can continue to operate in its current form, it holds multiple growth opportunities in the region.

According to Euromonitor International, value sales of e-commerce (goods) in Western Europe is projected to increase by a 10% CAGR between 2021 and 2026, reaching €EUR 715 billion. An opportunity for players to differentiate themselves amid the increasing competition could be specialising in financing a particular product category. An example could be luxury goods, sales of which might generate more value for point-of-sale financing than others.

Expanding beyond goods could accelerate the growth of BNPL in the region. In Australia, where the use of the service is already at a more advanced stage, BNPL has recently been made available for services. For instance, customers can ‘Dine Now, Pay Later’ with Afterpay at hospitality venues. Partnerships between BNPL players and service providers, from those in the travel or hospitality industries to utility providers, are also likely to gain importance in Western Europe going forward.

This Featured Article has been produced by Euromonitor. Rize ETF Ltd make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability or suitability of the information contained in this article.

Related ETF

PMNT: Rize Digital Payments Economy UCITS ETF

References

Euromonitor International, “The Disruptive Potential of Buy Now Pay Later in Western Europe”. Available at: https://www.euromonitor.com/article/the-disruptive-potential-of-buy-now-pay-later-in-western-europe

Subscribe to ARK Research & Insights